Not known Details About Paul B Insurance

Table of ContentsThe Definitive Guide for Paul B InsuranceSome Known Questions About Paul B Insurance.The 2-Minute Rule for Paul B InsuranceThe smart Trick of Paul B Insurance That Nobody is Discussing8 Easy Facts About Paul B Insurance Described

The idea is that the money paid in cases gradually will be much less than the overall premiums collected. You may really feel like you're throwing cash gone if you never sue, but having item of mind that you're covered on the occasion that you do suffer a significant loss, can be worth its weight in gold.Imagine you pay $500 a year to guarantee your $200,000 home. You have one decade of paying, and you have actually made no insurance claims. That comes out to $500 times ten years. This implies you have actually paid $5,000 for house insurance. You begin to question why you are paying a lot for absolutely nothing.

Because insurance coverage is based upon spreading the risk amongst many individuals, it is the pooled money of all individuals spending for it that enables the firm to build properties and cover insurance claims when they happen. Insurance policy is a company. It would be great for the firms to just leave rates at the exact same degree all the time, the fact is that they have to make enough money to cover all the prospective cases their policyholders may make.

Paul B Insurance - Questions

how much they entered premiums, they must revise their prices to make cash. Underwriting adjustments and also price boosts or reductions are based on results the insurer had in past years. Depending on what firm you acquire it from, you might be taking care of a captive agent. They sell insurance policy from just one business.

The frontline people you deal with when you acquire your insurance coverage are the representatives and brokers that stand for the insurance coverage firm. They a familiar with that business's items or offerings, but can not talk in the direction of other business' plans, pricing, or product offerings.

Paul B Insurance - Truths

The insurance policy you require varies based on where you are at in your life, what kind of assets you have, and what your long-term objectives and also tasks are. That's why it is crucial to put in the time to review what you want out of your policy with your agent.

If you obtain a car loan to purchase a cars and truck, and afterwards something happens to the car, void insurance policy will certainly pay off any section of your financing that typical automobile insurance coverage doesn't cover. Some lending institutions need their customers to carry void insurance try these out coverage.

A Biased View of Paul B Insurance

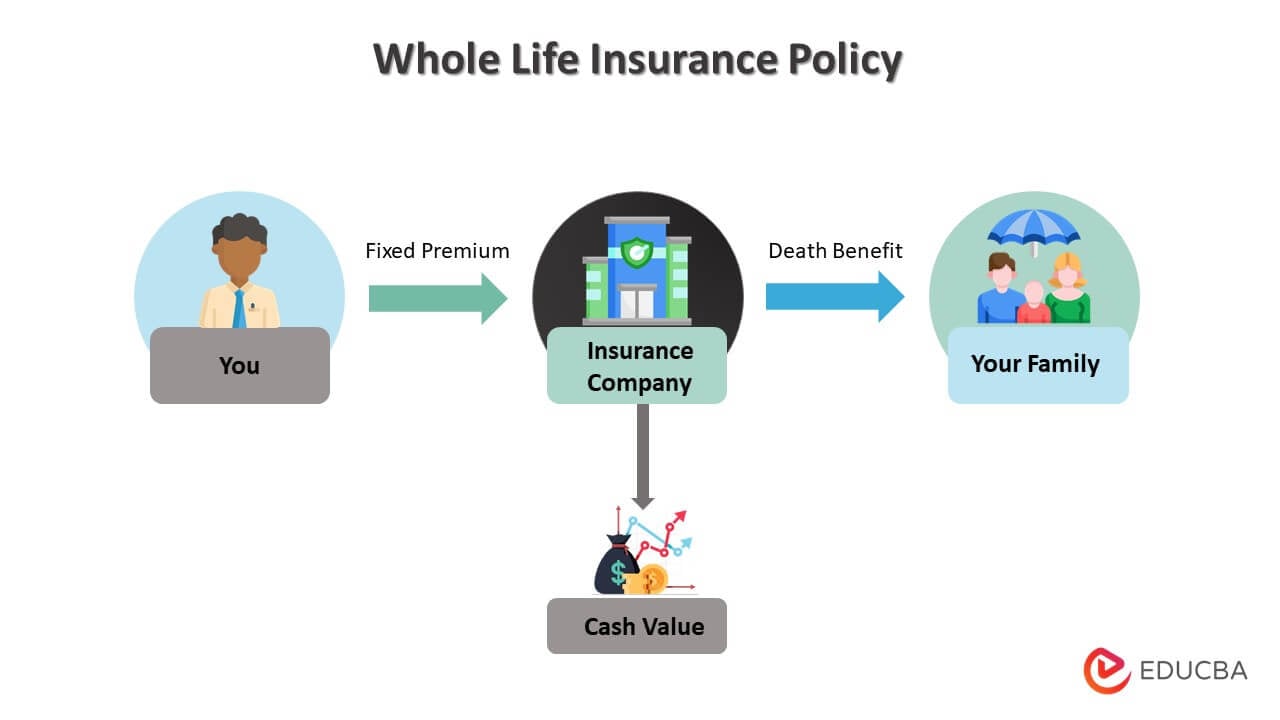

Life insurance coverage covers the life of the guaranteed individual. The policyholder, that can be a different person or entity from the insured, pays premiums to an insurer. In return, the insurer pays out an amount of money to the beneficiaries detailed on the policy. Term life insurance coverage covers you for a time period chosen at acquisition, such as 10, 20 or three decades.

If you don't die during that time, no person Bonuses gets paid. Term life is preferred because it provides big payments at a reduced cost than permanent life. It likewise supplies insurance coverage for a set number of years. There are some variations of normal term life insurance policy plans. Exchangeable policies allow you to convert them to long-term life policies at a higher costs, permitting for longer and also possibly extra flexible coverage.

Long-term life insurance policy policies develop cash value as they age. A section of the premium payments is included in the cash money worth, which can gain passion. The money value of whole life insurance policies expands at a set price, while the money go to this website value within universal plans can change. You can utilize the money value of your life insurance while you're still active.

The Only Guide to Paul B Insurance

If you contrast typical life insurance prices, you can see the difference. For instance, $500,000 of whole life protection for a healthy 30-year-old lady costs around $4,015 every year, typically. That exact same degree of coverage with a 20-year term life plan would certainly cost a standard of concerning $188 yearly, according to Quotacy, a broker agent firm.

Nevertheless, those financial investments feature more danger. Variable life is another permanent life insurance coverage alternative. It appears a great deal like variable global life yet is in fact various. It's an alternative to whole life with a fixed payout. However, insurance holders can use investment subaccounts to grow the cash value of the policy.

Right here are some life insurance coverage fundamentals to assist you better understand how coverage works. Costs are the settlements you make to the insurance policy firm. For term life plans, these cover the expense of your insurance coverage and administrative prices. With an irreversible plan, you'll likewise be able to pay money right into a cash-value account.